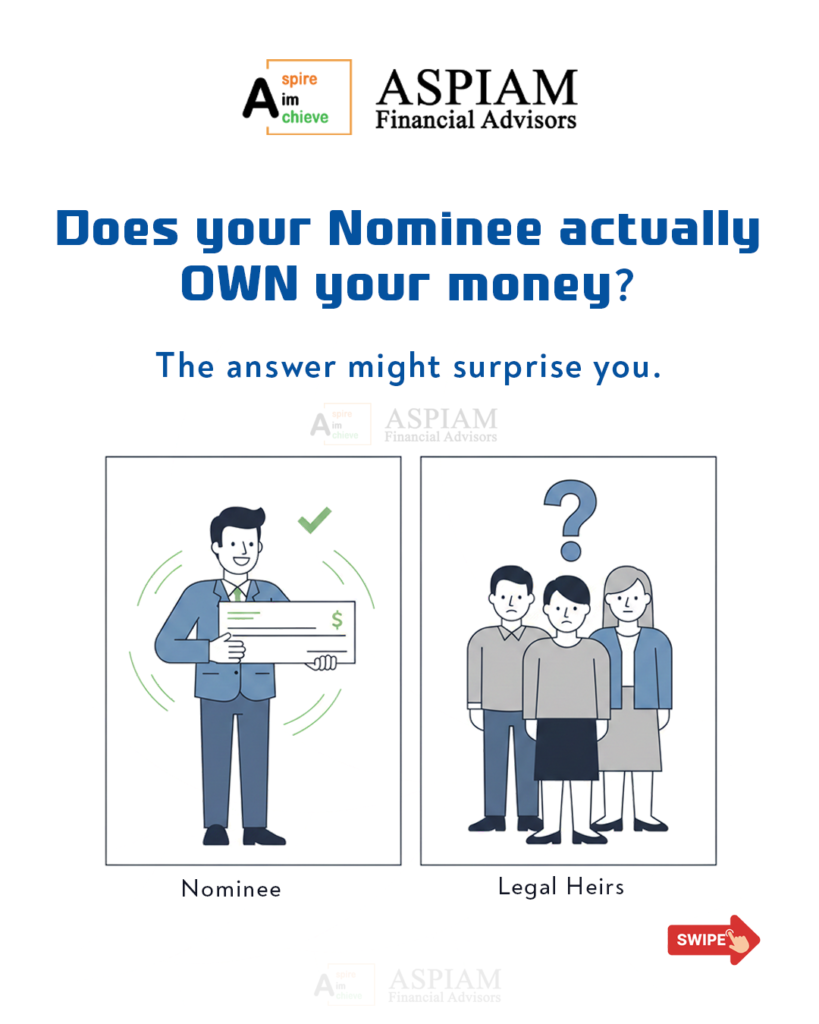

One of the most common and costly misunderstandings in personal finance is the belief that naming a nominee automatically makes that person the owner of the money. This assumption often leads to family disputes, delayed settlements, and outcomes that go completely against the original intent of the investor.

Let’s break this down clearly and practically.

First Things First: Who Is a Nominee?

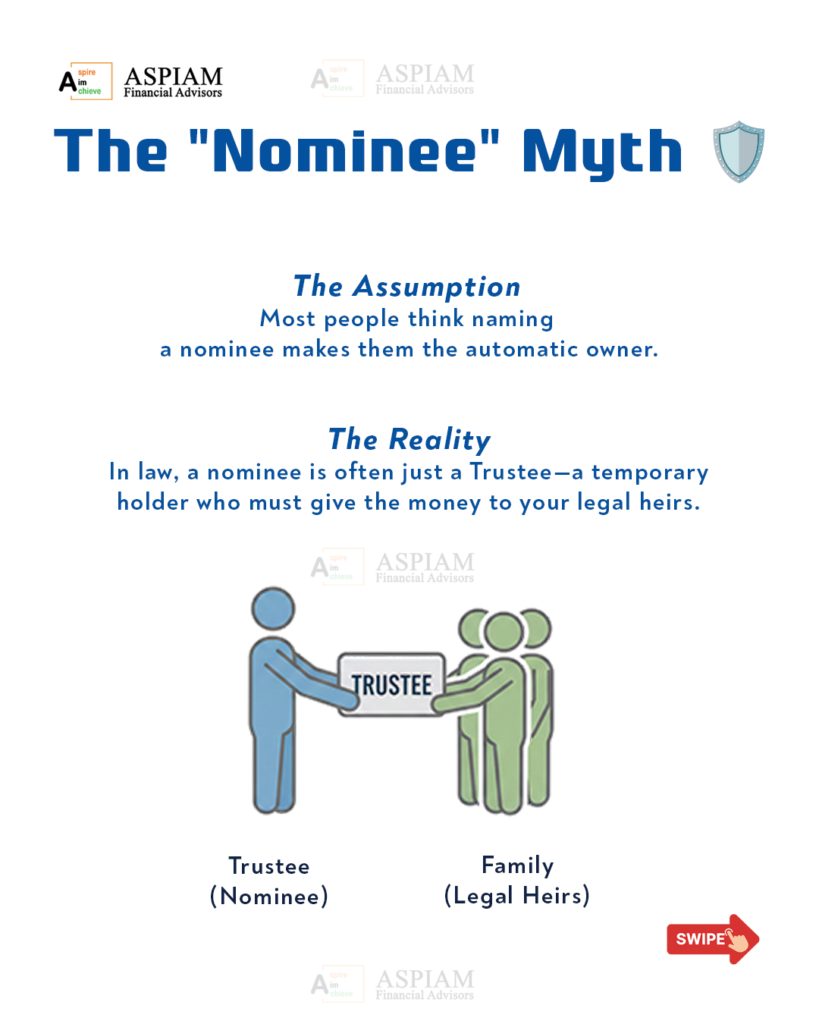

In law, a nominee is best understood as a person designated by an account holder to receive the account’s funds in the event of the account holder’s death. This ensures that the transfer of assets does not require any legal intervention.

The nominee acts as a trustee, holding the funds for the legal heirs/account holder who passed away. While the nominee gains temporary control over the funds, they are not necessarily the ultimate beneficiary. Appointing a nominee clarifies and reduces disputes, simplifying the settlement process for the bank and the account holder’s family.

The legal heirs (as per succession law or a valid will) are the true beneficiaries unless a specific statute provides otherwise.

A nominee is not the owner of the asset.

However, there are exceptions to this rule of Nominees also.

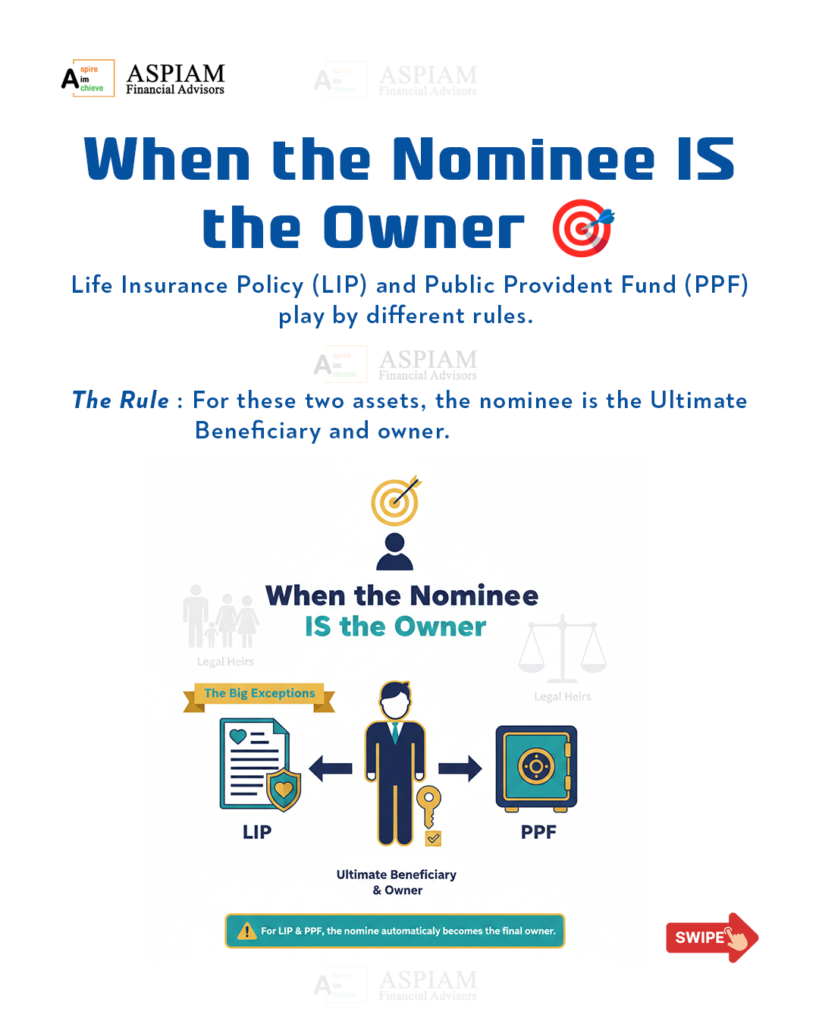

When it comes to Life Insurance Policies (LIP) and Public Provident Funds (PPF), the story is completely different.

Contrary to the straightforward definition of a nominee, the functions of a nominee in relation to LIP’s and PPF’s are the opposite.

A comprehensive chart and explanation for the same is provided below.

Let’s take a look at the role of a nominee in LIP and PPF;

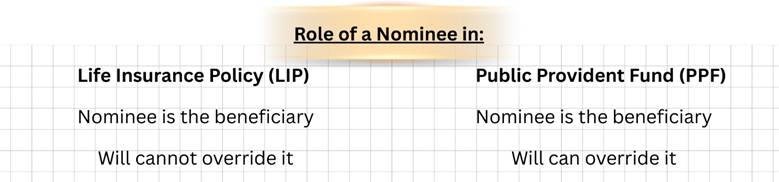

- Life Insurance Policy (LIP)

- A nominee in LIP is a beneficiary not only a holder of the asset. To put it simply, the nominee in this instance, becomes the owner of the asset upon the death of the account holder.

The nominee is the ultimate beneficiary.

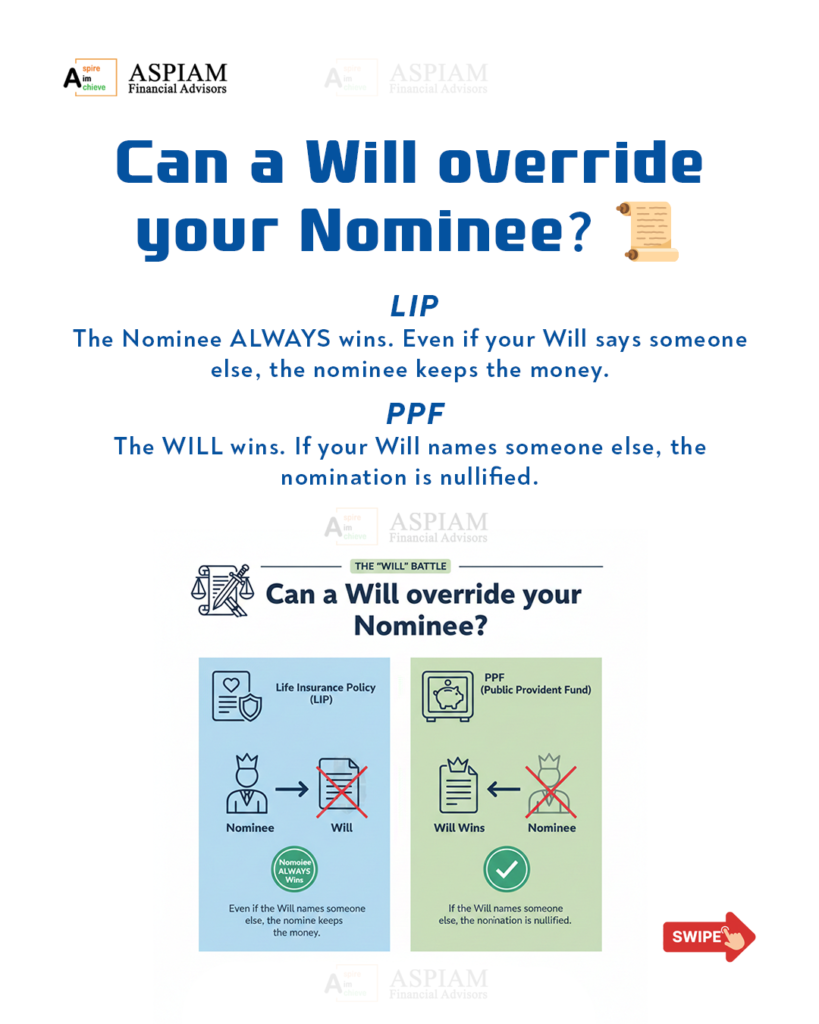

- Now, when a will comes into picture, the role of the nominee remains unchanged. The will could name a different person as the beneficiary of the asset but that will have no effect to the role of the nominee in a LIP whatsoever. The nominee regardless of what is written in the Will, remains the beneficiary after the death of the account holder.

- Public Provident Fund (PPF)

- As with LIP’s, nominee in PPF is a beneficiary and not only a holder of the asset i.e. the nominee will be the owner of the asset after the death of the account holder.

The difference in the treatment of nominee between LIP and PPF rises in the second condition reflecting the overriding of a will.

- In terms of PPF, even though the first condition suggests otherwise, the asset will go to the person stated as the beneficiary in the will in case a will exists and states a different person as the beneficiary after the death of the account holder.

In simple words, while a nominee in a PPF is typically considered the beneficiary after the account holder passes away, this condition will be nullified if the account holder has designated another person as the beneficiary of the asset in their Will.

Why This Difference Matters

Understanding this distinction can prevent:

- Family conflicts

- Litigation between nominees and legal heirs

- Assets being distributed contrary to your intentions

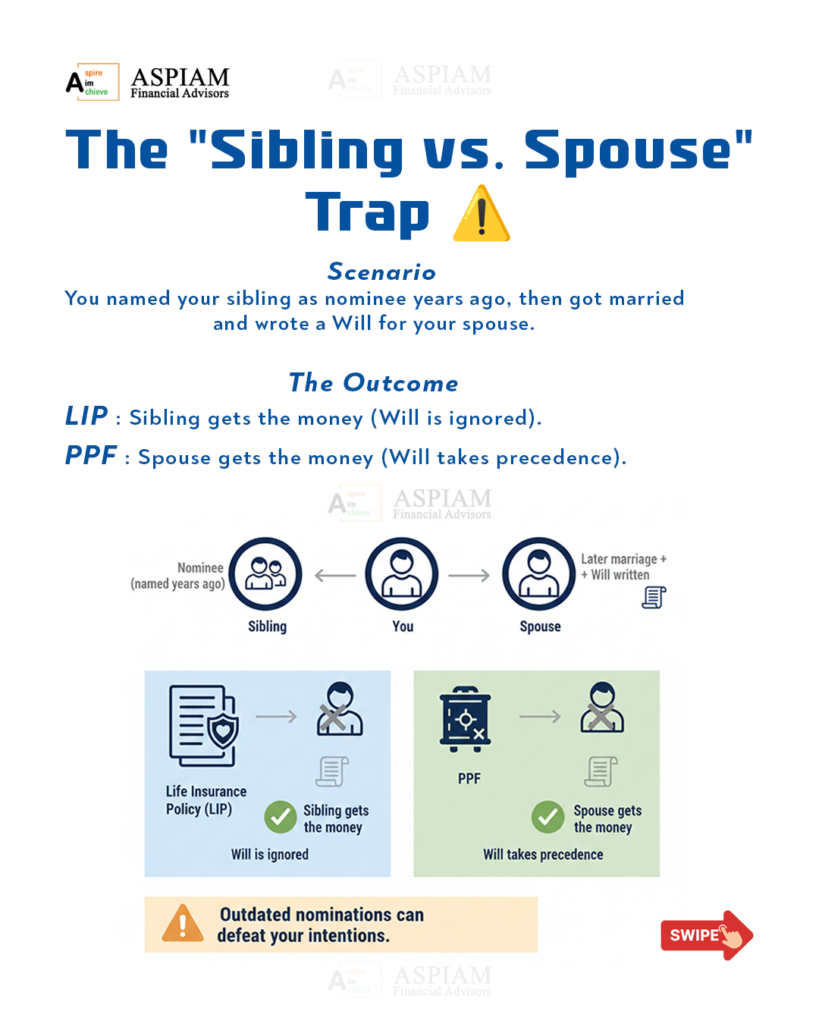

Consider this common scenario:

A person names their sibling as a nominee years ago. Later, they marry and write a will leaving everything to their spouse, but forgot to update nominations.

- For LIP: The sibling will remain the beneficiary and in turn will be the owner of the asset after the death of the account holder.

- For PPF: Although the sibling may be the nominee, the beneficiary as per Will take precedence over the nomination because it specifies that the spouse will acquire ownership of the asset upon the account holder’s demise. Therefore, the spouse will be the ultimate owner of the asset.

Practical Estate Planning Takeaways

- Nomination is not a substitute for a will it only ensures smooth payout and not final ownership.

- Align nominations with your will especially when life events like marriage, children, or divorce occur.

- Review nominations after major life events like marriage, children, divorce. Old nominations are one of the biggest causes of disputes.

- Understand product-specific rules Insurance and investment products follow differentlegal rules.Not all financial instruments treat nomination the same way.

The Bottom Line

The real question is not who receives the money, but who is legally entitled to keep it. The answer depends on the nature of the asset, the applicable law, and whether your estate planning documents are consistent.

A little clarity today can save your family years of confusion tomorrow.

In the end, it’s not about who receives the money, it’s about who the law allows to keep it.